China’s Hybrid Economy: How Central Direction & Free Markets Work Together

Snapshot of State-Owned and State Directed Sector

Understanding the Numbers

The anchor estimate: According to the World Bank, state-owned enterprises (SOEs) directly contribute approximately 23–28% of China’s GDP. This 25% figure represents output produced by firms where the state holds controlling ownership.

The “state-directed” economy is much larger: Beyond direct SOE output, the Chinese state exerts substantial influence through state banking (80% of banking assets), industrial policy, mixed-ownership enterprises, regulatory authority, procurement leverage, and Party committees embedded in corporate governance. This broader “state-directed” share is estimated at roughly 40% of GDP.

Recent developments: In March 2026, Reuters reported that China plans to inject $44 billion into its state banks as part of a broader recapitalization effort to deepen reform and boost technology financing. This reinforces the central role of the state banking system in directing capital allocation – a key mechanism of state-directed economic activity.

Methodological note: The categories shown above are not additive. They represent different metrics and scopes of state control across distinct sectors and measurement approaches. Figures are approximate estimates based on available data from the World Bank, OECD, Chinese official sources, and academic research (Stanford/SCCEI).

Executive Summary

China’s economy is neither a purely state-controlled system nor a free market. It is a deliberate fusion – a hybrid model where the state directs the “commanding heights” (banking, energy, telecom, transport) while private firms compete in manufacturing, technology, and services. This report explains how these two systems are moulded together to achieve national objectives: rising living standards, technological self-reliance, and stable growth.

The core insight: China uses state power not to replace markets, but to shape them – providing cheap capital, subsidized energy, and world-class infrastructure to competitive private firms that drive exports and innovation.

Part 1: The Two Engines of China’s Economy

What This Chart Shows:

| Sector | State Role | Private Role | Why This Split? |

|---|---|---|---|

| Banking | Controls 75% of assets | Shadow banking, fintech (Alipay, WeChat Pay) | Credit allocation = economic steering |

| Energy | 80% state-owned | Solar panel manufacturing (private) | Strategic resource security |

| Telecom | 90% state-controlled | Apps & services (WeChat, Douyin) | Data infrastructure = national security |

| Transport | 85% (rail, ports, highways) | Last-mile logistics (SF Express, JD) | Physical integration of national market |

| Exports | 15% | 85% private (Foxconn, private manufacturers) | Private firms excel at cost competition |

| Consumer Tech | 10% (Huawei hybrid) | 90% private (Xiaomi, Alibaba, Tencent) | Innovation thrives with competition |

| R&D | 35% (defense, space, basic research) | 65% private (commercial R&D) | Shared burden; state de-risks basic science |

Part 2: How State Direction Enables Private Success

The Support System Explained:

| Mechanism | How It Works | Impact on Private Firms |

|---|---|---|

| Cheap Credit | State banks lend to strategic private firms at 3-4% (market rate 6-8%) | Lower capital costs → higher competitiveness |

| Subsidized Energy | SOEs like Sinopec supply fuel/electricity below market cost | Reduces manufacturing costs for exporters |

| Infrastructure | State builds high-speed rail, ports, 5G networks | Private firms get world-class logistics without investment |

| Tax Rebates | VAT refunds on exports (up to 13%) | Direct price advantage in global markets |

| R&D Subsidies | Government grants for AI, EV, biotech | De-risks innovation; private firms commercialize |

| State Procurement | Government buys from strategic private suppliers | Guaranteed demand for emerging technologies |

Part 3: From Poverty to Prosperity – The Results

The Results of the Hybrid Model (1980 → 2025):

| Indicator | 1980 | 2000 | 2025 | Improvement |

|---|---|---|---|---|

| GDP per capita | ~$200 | ~$1,000 | ~$13,000 | 65x increase |

| Life expectancy | 67 years | 72 years | 78.5 years | +11.5 years |

| Urbanization rate | 19% | 36% | 68% | 49 pp increase |

| Poverty rate | 88% | 35% | <1% | Extreme poverty virtually eliminated |

| Internet users | 0% | 1% | 80%+ | Digital economy emerged |

Part 4: Technological Development – State + Private Collaboration

How Collaboration Works by Sector:

| Technology | State Role | Private Role | Outcome |

|---|---|---|---|

| Electric Vehicles | Subsidies, charging infrastructure, procurement (govt fleets) | BYD, Nio, Xiaomi – design, manufacturing, sales | China is world’s largest EV market |

| Solar Panels | Land, export support, initial R&D | Longi, Trina – production at scale (80% global share) | Solar now cheaper than coal |

| 5G Telecom | State-owned carriers (China Mobile) build networks | Huawei, ZTE manufacture equipment | 1.2 million 5G base stations nationwide |

| AI & Algorithms | Basic research funding, data access | Baidu, Alibaba, Tencent, Douyin – applications | Facial recognition, recommendation engines lead world |

| Semiconductors | $50B+ state investment, SMIC (state-backed) | Private design firms, Huawei’s HiSilicon | Reducing dependency on foreign chips |

| Space | State-owned CASC, military programs | Private satellite firms emerging | Tiangong space station, lunar missions |

| Batteries | R&D grants, export support | CATL, BYD (hybrid) dominate global supply | 60%+ global EV battery market share |

Part 5: The Steering Mechanism – How Government Sets Direction

The “Steering” Process Explained:

| Mechanism | How It Works | Example |

|---|---|---|

| Five-Year Plans | Set national priorities (e.g., “Made in China 2025,” “Dual Circulation”) | 14th FYP (2021-2025) targets AI, EVs, semiconductors |

| Credit Allocation | State banks direct capital to priority sectors | Green lending: $500B+ to renewables |

| Infrastructure Investment | Builds platforms for private sector growth | High-speed rail connects inland factories to ports |

| Strategic Designation | Official classification unlocks subsidies and support | “Strategic Emerging Industries” list |

| Procurement | Government purchases from targeted domestic firms | EV subsidies, government fleet purchases |

| Regulation | Licensing, standards, data rules shape market access | Data security law, AI regulation |

Part 6: The Hybrid Model in Practice – A Case Study

How an iPhone Gets Made: State + Private Fusion

| Step | State Role | Private Role |

|---|---|---|

| 1. Raw materials | SOEs extract rare earths, copper, aluminum | – |

| 2. Component manufacturing | State banks lend to supply chain firms | Foxconn, Luxshare, private suppliers assemble |

| 3. Energy & transport | SOEs (Sinopec, State Grid, China Railway) provide power and logistics | Private logistics (SF Express) for last-mile |

| 4. Export | Tax rebates (13% VAT refund), state-owned shipping (COSCO) | Private exporters handle documentation |

| 5. Global delivery | State-owned COSCO, China Southern Air | Private forwarders coordinate |

The Result: China produces 90%+ of all iPhones – not because the state owns Apple’s suppliers, but because state-provided infrastructure, credit, and energy make Chinese manufacturing the cheapest and most reliable in the world.

Part 7: What This Means for Non-Specialists

The Simple Version:

🏦 China is not a command economy. Private firms produce most of what you buy – iPhones, clothes, electronics, cars.

🚆 But it’s not a free market either. The state owns the railways, the banks, the power grid, and the telecom networks – the infrastructure that private firms rely on.

🔧 The fusion: The state provides cheap loans, subsidized energy, world-class ports and rail, and guaranteed export rebates. Private firms compete on cost, quality, and speed.

🎯 The result: Living standards have risen faster (1980-2025) than in any comparable period in human history. Extreme poverty has been virtually eliminated. China now leads in EVs, solar, batteries, and 5G.

🧭 The steering wheel: Five-Year Plans, state bank lending priorities, and strategic sector designations keep the economy moving toward government objectives – without the state having to own every factory.

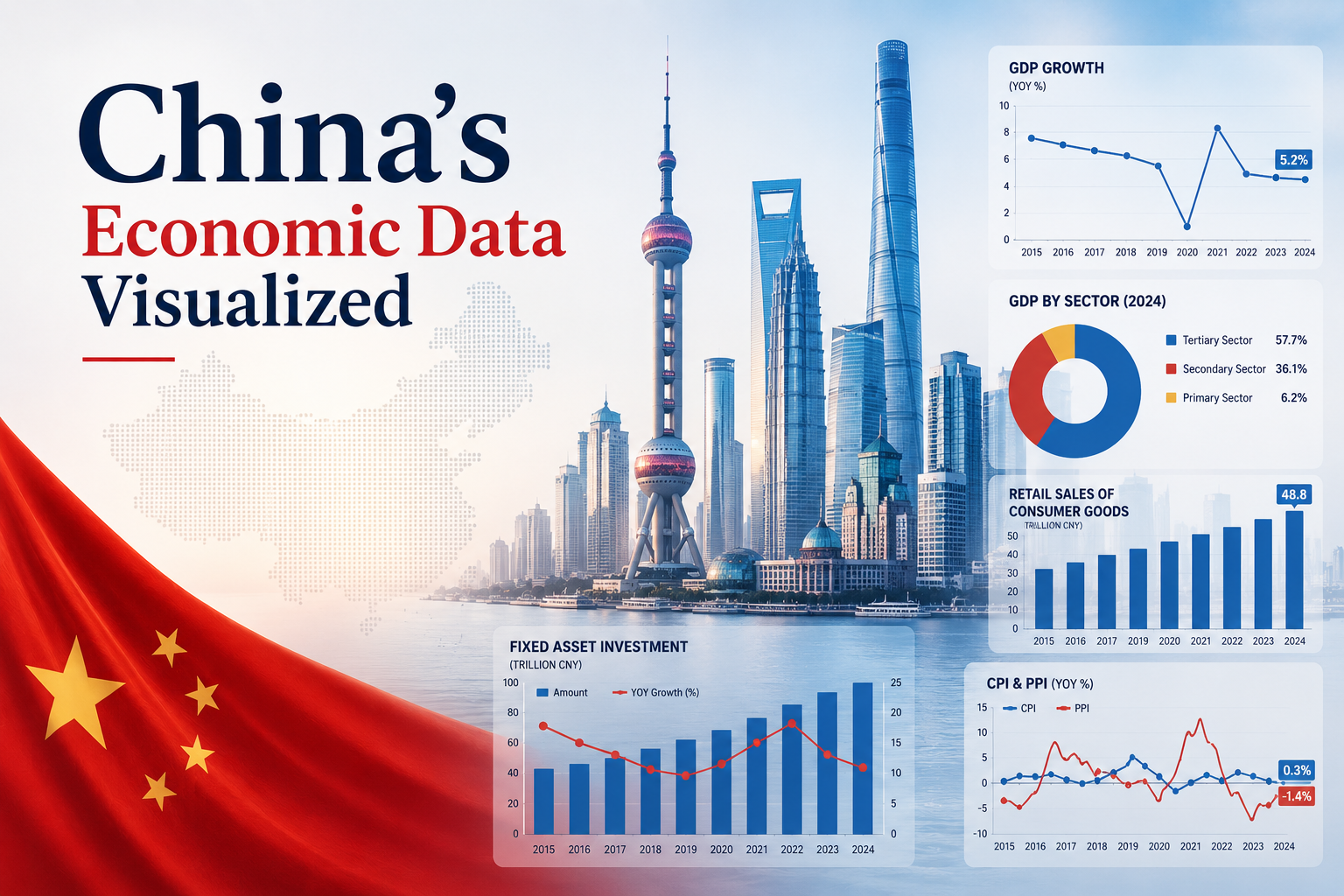

Return to: China’s Macro Data Visualized

Explore: Cityscape Investment Series: Unlock China’s Next-Gen Growth Engines

Explore: CEI’s Regional Economic Overview Series

Explore: China Logistics Reports

Sources & References

The following sources were used to compile the data, estimates, and analysis presented in this report.

Multilateral & Government Sources

- World Bank

“How Much Do State-Owned Enterprises Contribute to China’s GDP and Employment?”

SOE direct GDP contribution estimates (23–28% range) - International Monetary Fund (IMF)

www.imf.org/en/Countries/CHN

China economic outlook, hybrid economy working papers - OECD Economic Surveys: China

OECD Economic Surveys: China 2025

SOE reform, industrial policy, structural analysis - Reuters

“China to inject $44 billion into state banks, boost tech financing” (March 2026)

State bank recapitalization, financial system control

Chinese Official Sources

- 国务院国有资产监督管理委员会 (SASAC)

en.sasac.gov.cn

SOE performance data, reform announcements, sector statistics - 中国人民银行 (People’s Bank of China – PBOC)

www.pbc.gov.cn/en

Banking assets, credit allocation, monetary policy - 国家统计局 (National Bureau of Statistics – NBS)

data.stats.gov.cn/english

GDP, industrial output, living standards indicators - 中华人民共和国国家发展和改革委员会 (NDRC)

en.ndrc.gov.cn

Five-Year Plans, strategic sector designations, industrial policy

Academic & Research Institutions

- Stanford Center on China’s Economy and Institutions (SCCEI)

sccei.stanford.edu

Corporate capital estimates, state ownership research - Peterson Institute for International Economics (PIIE)

www.piie.com

China SOE reform, industrial policy analysis - Center for Strategic and International Studies (CSIS)

www.csis.org

Technology competition, state-directed innovation

Data & Market Intelligence

- CEIC Data

www.ceicdata.com

Historical economic indicators, sectoral breakdowns - Fortune Global 500

fortune.com/global500/

China SOE representation in global rankings - World Bank Open Data

data.worldbank.org/country/china

Poverty rates, life expectancy, GDP per capita trends

Additional Data Sources for Specific Charts

- Rising Living Standards Timeline

World Bank, NBS, UN Development Programme (UNDP) - Technology Collaboration Chart

IEA (EVs, solar), GSMA (5G), SIA (semiconductors), company reports - State-Private Sector Split

SASAC, NBS, PBOC, Fortune Global 500, academic research (SCCEI)

📅 Data as of May 2026

Figures are based on reported data from 2024-2025 and analyst estimates where official statistics are incomplete.

World Bank SOE GDP estimates reflect 2025-2026 analysis. Reuters state bank recapitalization reporting from March 2026.

Methodological note: Estimates for “state-directed” economic activity are based on multiple sources and represent conceptual ranges, not precise additive figures.

For detailed methodology, please refer to the original World Bank and SCCEI working papers cited above.