Introduction: The Visible War and the Invisible One

As the ceasefire in the Persian Gulf falters and the U.S. deploys more forces to the Strait of Hormuz and the Indo-Pacific region, analysts warn the conflict is part of strategy to sever China from its economic oxygen.

The logic, as I’ve stated in recent articles, is straight forward. The conflict is used as cover to implement a U.S. military blockade of the Strait of Hormuz. The blockade is then extended back to the Straits of Malacca and the vital chokepoints controlling entry to the South China Sea.

This analysis is not wrong. But it is incomplete. The real attack on China is simultaneously more complex and more subtle. It does not rely entirely on a prolonged, costly and logistically complex military operation that may ultimately fail militarily. The real plan is a meticulously constructed financial trap whose components are being assembled in plain sight using the architecture of an emerging multipolar financial system.

The visible military theatre—the carrier groups in the Gulf, the Western media narrative of overstretched US naval capacity, the carefully maintained façade of a transatlantic split—is not the operation. It is the cover story. The ostentatious “split” between Washington and Brussels reinforces the market’s assumption that the crisis is politically unsustainable and therefore temporary, depressing back-end futures prices and deepening the financial mirage. The real assault proceeds elsewhere. It is in the strikes on refineries and export terminals, in the sanctions architecture that forces Russia into the Petroyuan, and in the silent consolidation of the financial infrastructure that governs the price of oil. The carrier groups are the feint. The trap is the physical destruction of supply infrastructure and the financial arsenal of the United States.

This trap consists of three interconnected stages:

The Road Map

Stage 1: The Kinetic Squeeze. The long-term constriction of physical energy supply through the systematic destruction of production, processing, and shipping infrastructure. This creates the underlying condition of real, physical scarcity.

Stage 2: The Financial Mirage. The artificial manipulation of energy price signals, enabled by a concentrated ownership of the world’s primary oil futures exchange, the CME Group to hide the true severity of the scarcity, lulling China into complacency.

Stage 3: The Currency Ambush. A massive assault on China’s economic sovereignty in the form of currency warfare that exploits the dominance of the US dollar and, with devastating irony, weaponizes China’s own ambition to make the yuan a global petro-currency.

This is the blueprint for an invisible blockade.

Part 1: The Kinetic Squeeze – Manufacturing Scarcity

To set a trap, you must first shape the environment for it. In this case, the initial conditions are the deliberate, long-term constriction of global energy supply. What we are seeing around the world are not random acts of destruction. We are witnessing the systematic degradation of the world’s energy production, processing and logistical infrastructure.

The evidence from 2026 alone is staggering.

In the Persian Gulf, the damage has been strategic and precise. An attack on Qatar’s Ras Laffan LNG complex knocked out 17% of the country’s capacity for an estimated three to five years, sending a shockwave through global natural gas and fertilizer markets. In Saudi Arabia, strikes on the Ras Tanura refinery and the vital East-West pipeline have cut production and severely hampered the Kingdom’s ability to bypass the Strait of Hormuz. The UAE’s Fujairah terminal—a critical non-Hormuz export and bunkering hub—has been repeatedly attacked, driving up war-risk insurance and freight costs.

Meanwhile, a parallel but equally destructive campaign is being waged against Russia. Ukrainian drone strikes have become a persistent and devastatingly effective tool of energy warfare. They have shut down the NORSI refinery, crippled operations at the Ust-Luga gas complex, halted shipments at the Sheskharis terminal, and damaged pipelines leading to the Primorsk and Tuapse export hubs. A strike on the Druzhba pipeline in Ukraine even cut off oil supplies to Hungary and Slovakia for months.

The nominal, proximal, motivations of the actors on the ground may vary but the effect is cumulative. A growing amount of energy infrastructure—export terminals, pipelines, refineries, and tankers—has been damaged or disrupted this year resulting in a structural, long-term reduction in energy supply: oil, LNG, and shipping. Crucially, this physical scarcity is not a temporary blip. It is intended to be a structural feature.

Stage 2: The Financial Mirage – Hiding the Scarcity

With real-world supply under physical assault, the next stage is to ensure the financial markets do not accurately reflect this new reality. Instead, they must be made to send a false signal of calm and that this is a temporary disruption.

This is achieved through control of the world’s most important oil pricing mechanism: the CME Group, the exchange where the West Texas Intermediate (WTI) crude oil benchmark is traded. The price discovered in Chicago doesn’t just stay there. The powerful financial force of arbitrage acts as a transmission belt that almost instantly anchors oil prices around the world, including futures contracts traded in Shanghai.

If a trader can buy a barrel of oil on paper in Chicago for $60 and sell a contract for the same barrel in Shanghai for $65, they will keep doing so until the prices align. This makes the Shanghai International Energy Exchange (INE) a “net receiver” of the price signals established at the CME. If the CME price is artificially depressed, that false signal of ample supply is transmitted to China. Chinese refiners and government planners, looking at their own domestic market, are lulled into believing the current high prices are a short-term spike. They delay critical purchases and avoid drawing down strategic reserves.

This raises a critical question:

Who controls the price?

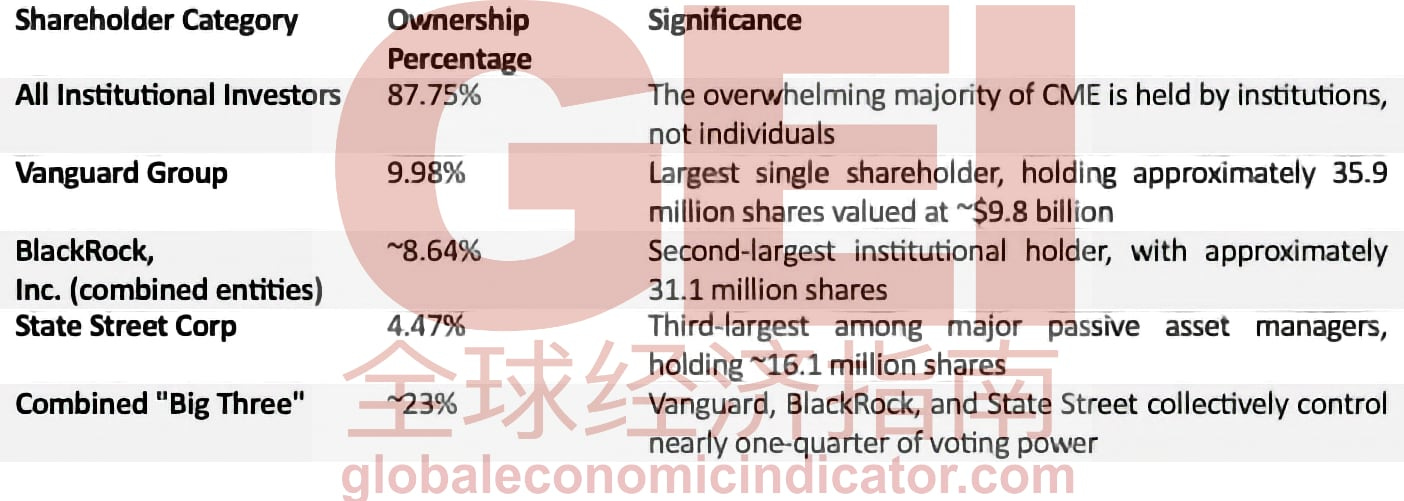

The ownership of the CME Group is extraordinarily concentrated among institutional investors, who collectively hold nearly 88% of the company. At the very top of this structure sit the “Big Three” asset managers: Vanguard (9.98%), BlackRock (~8.64%), and State Street (4.47%). Together, they control nearly one-quarter of the voting power of the exchange that sets the benchmark price for global energy.

This is not a conspiracy theory about traders in a dark room. It is about structural governance. The interests of these massive, passive fund managers are tied to the stability of dollar-denominated capital accumulation, not the efficient pricing of a physical commodity.

This structural control is about to become even more concentrated. On May 14, 2026, CME Group shareholders will vote on a proposal to eliminate the special board election rights of its Class B shareholders—the actual exchange members and physical market participants who have historically had a direct voice in the exchange’s governance. If passed, this vote will further consolidate power in the hands of the largest institutional investors, removing a critical check on the system and ensuring the financial “mirage” can be maintained with even less friction.

Stage 3: The Currency Ambush – Springing the Trap

The final stage is the most devastating. It is no longer about the price of oil; it is about attacking the financial foundation of the target itself—its currency and its finite reserves.

The Target: China’s Dollar Fortress.

The trap does not target China’s ability to print yuan. It targets its finite stockpile of US dollars, its foreign exchange reserves. In March 2026 alone, those reserves fell by $85.7 billion, the largest single-month drop in a decade. This is the ammunition China needs to defend its currency and pay for many of its essential imports.

When the “Physical Squeeze” hits and the “Financial Mirage” evaporates, China—and everyone else in the world—is forced to scramble for oil at the real, massively higher physical price. China will need to spend vast amounts of its precious dollar reserves at an alarming rate to fill the supply shortfall.

The collateral societal damage created by the global energy panic will be profound as energy prices double, perhaps quadruple, overnight. The ensuing physical shortages will cause widespread social dislocation especially in the Global South. In the West, COVID was dry run at population control in an era of economic upheaval.

The Battlefield: The Dual Life of the Yuan.

This assault is made possible by a unique and critical vulnerability China created for itself: the dual structure of the yuan market.

- CNY (Onshore): The yuan inside mainland China. It is a “high-walled fortress,” with its value strictly managed by the People’s Bank of China (PBoC) within a narrow 2% trading band.

- CNH (Offshore): The yuan that trades much more freely in global centres like Hong Kong. This is the “wild frontier,” with its direction of movement determined by global fear, greed, and supply and demand. (The PBoC does retain tools to manage this value and at time does intervene to prevent too large a spread with the CNY market.)

The Attack: Shorting the CNH.

This is when the trap springs. Speculators launch a sustained assault on the vulnerable, free-floating offshore yuan (CNH). They borrow massive amounts of CNH and immediately sell them, buying US dollars instead. This selling pressure causes the value of the offshore yuan to plummet relative to its tightly controlled onshore counterpart. This creates a price gap and a powerful incentive for arbitrage—buying the cheap CNH and using it in ways that put downward pressure on the stable CNY.

This forces the PBoC into a costly and potentially losing battle. To prevent the onshore yuan from collapsing, it must step into the market and spend its dollar reserves to buy back the offshore yuan and prop up its value. The trap forces China to haemorrhage the dollars it desperately needs to pay for its energy imports at the new, greatly inflated price.

The Amplifier: The Petroyuan as the Weapon of Choice.

Here is the trap’s final, most cunning irony. China’s grand strategy to insulate itself from dollar hegemony—the Petroyuan system—has become the trap’s primary amplifier.

China can print yuan to pay Russia and Saudi Arabia for oil. This seems like a shield. But Russia and Saudi Arabia are not charities. They must eventually convert a large portion of those yuan savings into US dollars or other hard currencies to pay for their own global trade. This conversion process adds a massive, additional wave of selling pressure on the offshore CNH market, accelerating the very currency collapse China is trying to prevent.

Russia, completely cut off from the dollar system and unable to act as a global stabilizer by buying yuan on the dollar markets a is forced to become a primary source of this destabilizing pressure. The system designed to protect China’s financial sovereignty is turned into the primary avenue of attack.

The Sanctions Pincer: How Brussels Armed the Trap

The EU sanctions regime against Russia is a critical structural component of the operation. The official rationale—degrading the Russian war machine—obscures an effect that aligns precisely with the trap’s architecture.

The first prong forces Russia into the Petroyuan. Successive sanctions packages systematically sever Russia’s access to dollar and euro-denominated finance. The result is the most dramatic forced dedollarization in history. By 2025, 99.1% of bilateral Russia-China trade was settled in rubles and yuan. Moscow’s central bank now holds yuan as a primary reserve. EU sanctions transformed the Petroyuan from a geopolitical aspiration into an operational necessity, flooding the offshore yuan market with the liquidity the currency ambush is designed to exploit.

The second prong ensures Russia is structurally incapable of defending the system it was forced to join. Excluded from SWIFT, its dollar reserves frozen, Russia cannot act as a global financial stabilizer. It cannot intervene to support the offshore yuan during a speculative attack. Instead, its energy companies—unable to hold dollars or euros—are compelled to amplify the pressure, converting massive yuan receipts into usable currency and adding directly to the selling pressure on the CNH.

EU sanctions simultaneously deepen the Petroyuan system and ensure its largest participant acts not as a stabilizer but as an accelerator of the crisis. The pieces fit.

There is no smoking gun or secret plan discovered in a hidden safe, but the circumstantial evidence strongly suggests that the creation of the Petroyuan in itself was not an unintended consequence of Western sanctions but a deliberate, multi-year operation to construct the financial architecture that would later become the primary avenue of attack.

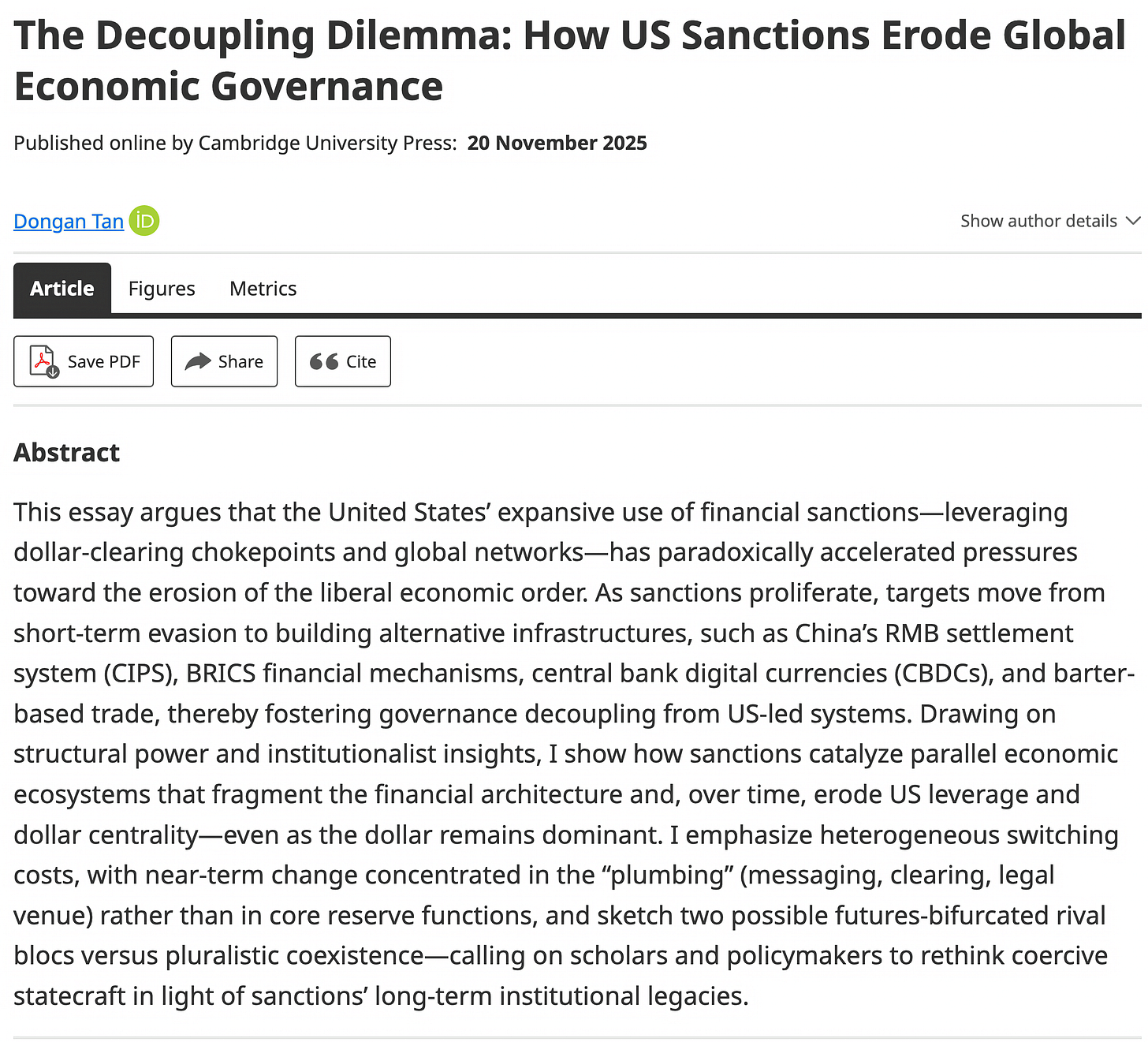

Numerous academic research papers confirm the structural dynamic. A 2025 Cambridge University study argues that US financial sanctions have “paradoxically accelerated pressures toward the erosion of the liberal economic order,” as targets “move from short-term evasion to building alternative infrastructures, such as China’s RMB settlement system (CIPS)”. Analysts note that sanctions have created “a permanent geopolitical financial split, accelerating global de-dollarization”.

West did not just fail to stop the rise of the Petroyuan—it actively engineered its creation. By cutting Russia off from SWIFT and freezing its dollar assets, the West left Moscow with no choice but to embrace the yuan as its primary foreign currency. Russia “was excluded from the SWIFT payment system” and faced “restricted use of dollars and euros,” forcing its “pivot toward the Chinese yuan as a lifeline“. The Petroyuan was not a Chinese victory; it was a Western trap.

The Tragic Irony

The People’s Bank of China spent decades fortifying the yuan against a currency attack behind strict capital controls. The central logic was that no speculative assault would be able to breach the defences. So, the strategy was to lure the defenders outside into the open.

The internationalization of the yuan in the form of the Petroyuan was the bait.

When Russia intervened in Ukraine the collective West responded with a financial firestorm. Sanctions, SWIFT exclusion, asset freezes. By doing so they created an irresistible temptation for China to internationalize its currency in the form of the Petroyuan. China believed it was building the financial infrastructure for a multipolar world; in reality they were inadvertently creating a financial battering ram that would be used to try and breach the walls of the onshore yuan fortress.

With every barrel purchased more ammunition is handed to the enemy. The more oil is traded in yuan the less defence the walls of capital controls offer. The trap is now fully armed.

The physical scarcity engineered in Stage 1 forces China to print more yuan to pay for expensive energy. The financial mirage of Stage 2 ensures China delays building its defences. And the currency ambush of Stage 3 unleashes the speculative attack on the exposed CNH, forcing the PBoC to spend its dollar reserves—its own siege supplies—to defend a currency it was deploying beyond its walls.

The fortress was never breached. It was emptied.

The Architect’s Resume: Bessent and the Currency Wars

Scott Bessent’s presence as Treasury Secretary directly supports this thesis. The current plan requires an individual who understands, at an operational level, how to identify the fatal flaw in a sovereign financial system and apply concentrated pressure until it breaks. Bessent’s career is a catalogue of precisely this skill.

In 1992, as a young partner at George Soros’s firm, he was dispatched to London where he identified a critical vulnerability: the British housing market was dominated by floating-rate mortgages, meaning the Bank of England could not raise interest rates to defend the pound without bankrupting millions of homeowners. This insight gave Soros the confidence to amass a $10 billion short position against sterling.

The result was “Black Wednesday,” the pound’s forced ejection from the European Exchange Rate Mechanism, and a profit of over $1 billion for the fund—costing British taxpayers billions and toppling the government of Prime Minister John Major.

Two decades later, in 2013, Bessent was the chief investment officer who personally orchestrated Soros Fund Management’s short against the Japanese yen, a trade timed to exploit the Abe government’s quantitative easing program that generated nearly $10 billion in profit. His method in both cases was identical: identify a policy-driven distortion, wait until the target’s capacity to respond is constrained, and then strike with leveraged precision.

That the architect of the “Black Wednesday” attack and the “Abe Trade” now occupies the office of Treasury Secretary—with authority over sanctions, financial stability oversight, and dollar policy—is precisely what one would expect if the blueprint we have described were being implemented.

The Dry Run: Iran as the Test Case

Before this kind of complex financial operation is deployed it is tested and refined. The collapse of the Iranian rial between late 2025 and early 2026 looks like such a test. It was a miniature, accelerated version of the three-stage trap about to be sprung against China—a proof of concept conducted on a vulnerable petro-state whose economy was already hollowed out by decades of sanctions and a summer of war.

It followed the similar blueprint, compressed into months rather than years. The kinetic squeeze was the twelve-day war with Israel in June 2025, strikes hit the Fajr Jam Gas Refinery and a processing unit at Phase 14 of the South Pars field, the world’s largest gas reservoir. This degraded energy infrastructure created the physical vulnerability. The financial squeeze followed in September 2025, when European powers activated the UN “snapback” mechanism restoring all pre-2015 sanctions and severing Iran’s remaining access to hard currency.

The currency ambush unfolded with devastating speed. Before the war, the dollar traded at approximately 600,000 rials on the open market. By the end of 2025, the rate had passed 1.4 million. By January 2026, it crossed 1.6 million. Food inflation reached 89.9 percent year-on-year, with prices for oils and fats alone surging over 50 percent in a single month. By March 2026, year-on-year food inflation had climbed to 112.5 percent.

COVID-era Proof of Concept

Before the Iranian rial was sacrificed as a trial run, an even more foundational test had already been conducted. In April 2020, with the global economy in pandemic-induced paralysis, the price of a barrel of West Texas Intermediate crude oil fell to negative $37.63.

The critical point is not simply that prices went negative. It is why they went negative. The futures market catastrophically failed to perform its most essential function: to adequately price future demand destruction.

In the weeks leading up to the collapse, futures prices remained stubbornly disconnected from physical reality. Storage at Cushing, Oklahoma—the delivery point for WTI contracts—was rapidly filling. Anyone with eyes on the ground could see the glut. Yet the futures curve failed to signal the severity of the coming imbalance. When the May contract approached expiration, traders who had no ability to take physical delivery of oil were trapped. They had to pay buyers to take the contracts off their hands. The market did not gently reprice risk over time; it violently seized at the last possible moment.

The CME Group, owner of the exchange where this benchmark is traded, had quietly issued an advisory notice on April 8, 2020, confirming that its systems had been reconfigured to accommodate negative pricing. Twelve days later, the May WTI contract collapsed. The event proved three essential principles that underpin the current trap:

- First, the exchange could fundamentally alter the rules of the game without triggering systemic collapse.

- Second, passive investment vehicles like the United States Oil Fund (USO) could be weaponized as sources of mechanical selling pressure.

- Third, regulators would ultimately decline to assign meaningful blame, with the CFTC’s investigation drawing criticism even from its own commissioners as “incomplete and inadequate.”

Most importantly, the negative price shock established a critical precedent: the futures market could be allowed—or engineered—to fail at its primary task of forward price discovery. A market that cannot accurately signal future supply and demand conditions is not a market at all. It is a mechanism for transferring wealth from those who trust its signals to those who understand its vulnerabilities.

This precedent is directly relevant to the current trap. Where the 2020 failure was a failure to price future demand destruction (oversupply), the current configuration is a failure to price future supply destruction (scarcity). The mechanism is identical; only the direction is reversed. In both cases, the futures curve sends a false signal of calm, lulling market participants into complacency until the physical reality violently reasserts itself.

The negative price shock was, in essence, a permission slip for what was to come—a demonstration that the world’s most important commodity pricing mechanism could be decoupled from physical reality without consequence for those who controlled it.

COVID was simultaneously test-run at manipulating futures markets in real time and also for managing domestic populations through the period of imposed, devastating economic fallout that accompanies the plan.

Testing the Hypothesis: What the Evidence Shows

A credible hypothesis must generate testable predictions. So, let’s figure out what we should see in the data if the hypothesis is correct:

The cumulative picture is striking. The physical market is screaming scarcity while the paper market signals calm. The governance of the world’s primary oil pricing mechanism is being consolidated precisely as the crisis unfolds. The media is filled with false promises of a return to normal and U.S. military prevarication.

None of this constitutes a smoking gun. Each data point, taken in isolation, has a plausible alternative explanation. But the hypothesis does not rely on any single signal. It predicts that all these signals should appear simultaneously, as interconnected components of a single operation. That is precisely what the evidence shows.

Historical Echoes: The Plaza Accord

In 1985, the world’s five largest economies agreed to coordinated currency intervention at New York’s Plaza Hotel. The objective was to depreciate the overvalued US dollar. The result, for Japan, was catastrophic.

As a result of the Accord and subsequent poor policy reactions the Nikkei lost over 75 percent of its value across the subsequent decade. Real estate fell for fourteen consecutive years. Japan entered its “Lost Decades”—thirty years of stagnation from which it has only recently begun to emerge.

The parallels to the present are direct. Japan in the 1980s was pursuing yen internationalization, seeking to establish its currency as an alternative to the dollar. China today is pursuing the same objective through the Petroyuan system. In both cases, the ambition to challenge dollar hegemony triggered a similar defensive response from the US financial establishment. The blueprint endures.

The Feint: Why the Visible Military Theater Is a Misdirection

Western media coverage has fixated on a single narrative: the United States lacks the capacity to enforce a meaningful blockade of Hormuz, let alone the sea lanes to Malacca. The analysis is not inaccurate. It misses the point entirely—and in doing so, serves the operation’s purpose.

The visible military posture is a feint. The carrier groups are there to command attention, ensuring adversaries fixate on physical chokepoints while the real operation proceeds elsewhere. The trap does not require a successful naval blockade. It requires only that the destruction of energy infrastructure continues and that the financial architecture functions as designed. Tankers can keep sailing. Refineries and export terminals cannot keep operating. That asymmetry is the foundation the trap is built on.

The same logic applies to the spectacle of NATO disunity. The public “split” between Washington and Brussels is not alliance fracture. It is a necessary component of the illusion. A crisis that appears politically unsustainable reinforces the market’s assumption it will be short-lived, depressing back-end futures prices and deepening the false signal of temporary disruption. The real operation is not the ships. It is the strikes, the sanctions, and the consolidation of the financial infrastructure that governs the price of everything.

The Counterpoint: Why China Is Not Japan

The parallels between the Plaza Accord and the current trap are striking, but they obscure critical differences. China is not Japan. Its vulnerabilities are real, but its defences are substantial, and the outcome of this operation is far from set in stone.

First, China is a legitimately sovereign country and has genuine policy autonomy. Japan was and is a security client of the United States, hosting American military bases and operating within a US-dominated alliance structure. When Washington demanded yen appreciation, Tokyo’s room for refusal was narrow. China is a fully sovereign nuclear power with an independent foreign policy and a centrally planned economic apparatus. It can say no.

Second, capital controls do provide a genuine defence. Japan’s financial liberalization in the 1980s allowed speculative capital to flood ebb and flow freely, inflating and then collapsing its asset bubble. China maintains a tightly managed capital account. This is precisely why the trap targets the offshore yuan market—the controls force the assault through a single, narrower channel that the PBoC can defend with greater focus.

Third, China’s domestic market absorbs shock. Japan’s post-war economy was fundamentally export-dependent, leaving it acutely vulnerable to currency appreciation. China’s 1.4 billion consumers provide an internal demand base of sufficient scale to partially cushion external blows. An energy crisis will badly damage its economy, but it will not break it.

Forth, and importantly, China knows what happened to Japan. Chinese policymakers have spent decades analysing the Plaza Accord. This does not make China immune, but it means Beijing enters this crisis with its eyes open to the dangers of panic-driven policy.

The trap is extremely sophisticated and has been years in the laying. Its architects have studied history. But so has its target. The critical variable has not changed since the Plaza Accord: the trap is most effective when the target nation responds to external pressure with suboptimal policies choices. How China responds will determine whether this operation succeeds or accelerates the multipolar transition it was designed to prevent.

Conclusion: The Grand Illusion

The coming war is not a war that will be fought primarily with tankers, destroyers and naval mines. It is a war being fought primarily with algorithms, arbitrage, and structural financial power.

The plan creates a grand illusion: the appearance of a short-term, temporary disruption while engineering a massive, global energy shock to force China into an impossible dilemma: whether to divert the dollar reserves it needs to subsidize its energy imports to defend the value of the offshore yuan; or let the yuan devalue and import a tidal wave of inflation that erodes economic and social stability.

The pieces are not hidden. They are visible in the burning refineries of Russia and the Persian Gulf, in the ownership filings of the CME Group, in the presence of Scott Bessant at the Treasury and in the quiet, accelerating drain of China’s foreign exchange reserves. The trap is set, and the world is watching it spring.

In the next article, I’ll explore the options China has to defend itself and the possible retaliatory measures that can be deployed.

For the latest updates follow us on Telegram, X (Twtter) or subscribe on Substack.